Based on remarks at the OECD Chief Economist Talk Series, Paris, 23 April 2020

and a Research Webinar at the BIS, 13 May 2020Luiz Awazu Pereira da Silva

1. Introduction: about global risks

Policymakers are increasingly concerned about climate-related risks as manifested in more frequent and more destructive weather catastrophes, causing significant losses to people, firms, banks and insurance companies, and hence posing a growing threat to financial stability. This is one reason why central banks and supervisors have put climate change on their agenda. In the last two years, 65 central banks and financial supervisors have joined the Network for Greening the Financial System (NGFS) (as of 16 April 2020). But climate risks have also caught the attention of society as a whole, as well as that of large investment firms and asset managers. Our book The Green Swan develops this concept, as inspired by the famous Black Swan of Nassim Nicholas Taleb. Then, from the end of last year, we have had to deal with another negative global externality in the form of the Covid-19 pandemic. This is another global risk, in addition to climate change, that was neither fully considered nor priced. For both, there is a discrepancy between how scientists worry about these global risks and how most risk managers and economists currently integrate them into costs and prices. Therefore, both pose the question of how to reconcile these different approaches to dealing with them.

In what follows, we explain the common intuitive thread between a Black Swan and what we call a Green Swan: their common mispricing of global risks but also their differences. Due to the global nature of Green Swans, we advocate more cooperation to prevent them, which will require changes in models and mindsets in many directions and by many agents (central banks, governments, civil society, the private sector etc). Since these global risks threaten financial stability, the current mandate of central banks plays an important role but no single actor has a silver bullet to solve this crisis. Thus, global risks call for a new landscape of cooperation among players, including central banks. Finally, I provide some personal additional thoughts on global negative externalities (global risks) and suggest that Covid-19 could be classified as a Green Swan. I discuss below in more detail that both climate-related risks and more frequent pandemics are related to changes in our natural environment and our ecosystems (see Box 1), directly affecting human lives. The important point is perhaps less the taxonomy but the need for coordinated collective action to address these global risks. In our current frameworks, most of these global risks end up being mostly considered ex post, after some irreversible tipping-point. However, financial markets are become increasingly aware of these global risks.3 So, using Covid-19 as another example of a global risk, what lessons should we draw from the current crisis to better prepare our socio-economic organisation? The major issue is the cost of prevention to reduce these risks, and looking at the current loss of global welfare (see Graph 1), it now seems that is worth considering some form of insurance. More generally, the effects of global risks such as pandemics illustrate the trade-off between efficiency and resilience. Finally, the lessons should help us to engineer a recovery that mitigates, or at least will not aggravate, the risks of new climate-related Green Swans.

2. Black and Green Swans: exploring global risk categories, what they have in common and what is different

The Macmillan Dictionary offers the following definition: “A green swan is a climate event that is outside the normal range of expected events. Green swans are different from black swans because there is some certainty that climate change risks will one day materialize.”

The damage caused by Black and Green Swans to societies and their economies have a lot in common. (i) They are unexpected by most agents, who look at the past as being a good proxy of the future; (ii) both feature non-linear propagation, caused by and triggering multiple destructive forces that feed-back on each other; (iii) their effects cascade into multiple sectors and countries simultaneously; and (iv) they are of a very large magnitude and intensity. From a strictly economic policy viewpoint, climate-related risks and pandemics such as Covid-19 produce similarly devastating effects on both the real and financial sectors, causing recessions, unemployment and a large depreciation of value across all asset classes (for some cost estimates for the global sudden stop, see Graph 1).

Recent BIS research confirms that the short-term costs of Covid-19 are significantly higher than for past epidemics, precisely because of the global sudden stop due in part to containment measures. The current estimated impact on global GDP growth for 2020 is around –4%, with significant downside risks.5 Compounding that, there are also risks of spillovers and spillbacks across countries due to imperfect coordination in confinement policies and to the transmission of the shocks through existing traditional trade and financial integration arrangements.

Another striking common feature is that they both entail large negative externalities at a global level. Hence, neither the private sector nor government can adequately “price” the associated risks in the costs of our goods and services. For instance, the macrofinancial risk of global pandemics has previously been at best minimised if not ignored. Despite past outbreaks such as H1N1, SARS and Ebola, their full consequences were not properly considered. Because they did not cause a global sudden stop, they were seen as a tail risk event that would remain manageable. Of course, striking the right balance in assessing the potential severity of diseases is a very difficult task. And indeed the 1918 Spanish flu was a once-in-acentury episode, while Ebola was contained within its region of origin. But most scenarios concerned diseases with high levels of contagion and relatively mild lethality, or with high lethality but only very limited transmissibility. Neither public health nor economic systems were prepared for the risk of a Covid-19 scenario, no insurance market had developed to hedge this risk and no financial market had fully priced the possibility of its occurrence, despite the role of regulators in building multidimensional stress tests.

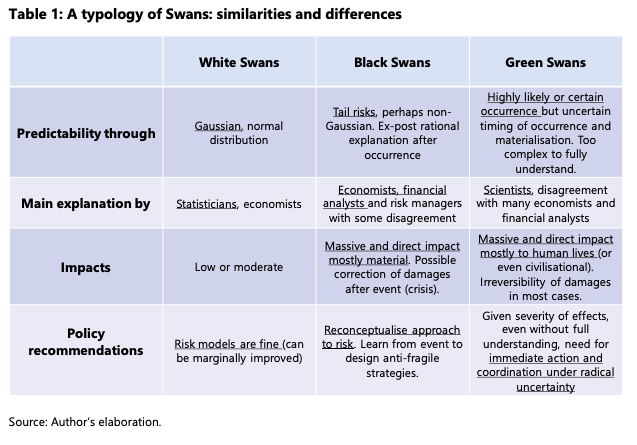

Yet these two major global risk categories differ in important respects. The first difference is about predictability. Green Swans are events that are either extremely likely or quite certain to occur (pandemics and climate change), as confirmed by our best science today. Yet, their exact timing (when) and form of occurrence (where and how) are unknown. By contrast, Black Swans do not manifest themselves with this high likelihood or quasi-certainty. They are exogenous tail-risk events (although this tail may not even be part of a classical Gaussian bell curve). Black Swans are severe and unexpected negative events that can only be rationalised and explained after their occurrence, as in the case of the Global Financial Crisis. Finally, the predictability of both Black and Green Swans will always differ from the modelling of risks encountered in traditional risk management (ie normal distribution, see Table 1).

The second difference is about who provides the main explanation for these events. For Blacks Swans, the field is mostly occupied by economists and financial analysts. For Green Swans (pandemics and climate change), the main underlying literature comes from scientists, even if economists are needed to assess the economic and financial impact. That is because we are dealing with studying events that are, directly or indirectly, related to the various ways through which our actions affect our natural environment and how this creates new local and global risks for us (see Box 1).

The third difference is about their respective impact. The effects of Green Swans are in most cases irreversible (ie the damage done to our environment), whereas Black Swans such as the Global Financial Crisis (GFC) have effects that are long-lasting but can eventually be corrected. A fourth difference between Black and Green Swans resides in the way we derive policy recommendations to prevent their occurrence. It is not enough to change our approach to risk and abandon the bell curve as a guide to discussing risk tolerance for events such as Black Swans. Finally, perhaps the major difference is that Green Swans relate to changes we make to our environment and our ecosystems that pose a massive, direct and irreversible threat to human lives, unlike Black Swans, whose effects are mainly on the real and financial economy. Indeed, what is at stake with climate change are the resources and opportunities available for future generations. Faced with sets of events that are complex, subject to radical uncertainty but with the likelihood of a massive future impact, Green Swans call less for improvements in risk modelling and more for decisive and immediate action and coordination. I will explain what type of coordination in the next section.

3. More (not less) global cooperation and coordination are needed

Due to the complexity of Green Swans, no single actor, whether national or global, will have a silver bullet for their solution. By definition, global negative externalities require coordinated global action. In the case of climate change, the NGFS has played an important role in increasing awareness, and it has started to coordinate with national treasuries, civil society, NGOs and, of course, multilateral development banks (MDBs). The responses to the Covid-19 crisis have shown a promising degree of fiscal and monetary policy coordination at both local and global levels. The speed of contagion in successive regions has created incentives to cooperate or at least to fight the crisis simultaneously across countries. There are also many new policy recommendations in a growing literature. These range from implementing much needed initial public health measures to use decisively all available macroeconomic tools to reduce the economic and financial fallout of the Covid-19 crisis, a sort of “whatever it takes” moment for economic policy.8 Existing national and global frameworks, together with the existing relationships between central banks, have also helped. Nevertheless, there have been many calls to further strengthen some of our global and regional safety nets (eg international financial institutions and regional arrangements). Similarly, new central bank-led facilities (swap lines, liquidity provision) have been an important element for liquidity provision in hard currency. But an even more encompassing approach is necessary.

First, more global coordination is needed to foster change in methodologies and mindsets to deal with this type of global risk. We need to put more effort into global cooperation to research and better understand climate risks, and to open up possible solutions. For example, using historical data to model the interaction between global warming and climate risks is not a good predictor for future risks, tipping-points and economic damage. Pandemics may seem to be a better explored territory in terms of their epidemiology, but we have also seen how the economic impact is hard to assess. This is because we are dealing with non-linear phenomena, exponential and complex transmission mechanisms, together with cascading effects into many sectors and countries. Therefore, risk management needs to be forward-looking and scenario-based. Further, we might need to complement this with some sort of broader holistic approach because even the best scenario analysis remains limited when seeking to identify all the possible ways in which Green Swans could emerge and how they will spread. This will require an “epistemological rupture” in our modelling strategies.

In addition to changes in modelling approaches, we need to find the most appropriate way to internalise these risks in prices and additional costs. For example, in order to take into account climate-related risks, it is necessary to put in place, inter alia, an adequate carbon price. But this is probably not sufficient, as suggested by the 2017 Stern–Stiglitz report. The classical emphasis on carbon pricing cannot be a silver bullet that will address the full complexity of climate events. It will therefore need to be accompanied by regulatory interventions and other public policies. This is due to uncertainty, imperfect information and all the ramifications that inevitably surround the final outcome of any investment in innovation. We need many other changes in behaviour and production processes. We also need to reflect on how far the risks of pandemics such as Covid-19 could somehow be translated into preventive measures whose costs could be incorporated into the final prices of our global value chains, our external transactions, our airplane tickets, our logistical and communication costs etc.

These are difficult issues but doing nothing amounts to continuing to believe that we can increase the span and efficiency of our global networks of production and consumption without incurring any additional risk. But these networks have failed to take into account risks with huge global negative externalities.

Second, we already knew that, when dealing with climate-related risks, there are many agents with whom coordination is needed. For example:

• Coordination is, of course, needed first between and within governments, so that their policy mix is adapted to, among other things, a fiscal policy with a lower carbon footprint, the promotion of sustainable investments and a longer-term view of returns on investment projects. For instance, some financial institutions have integrated sustainability investment criteria into their own portfolios (eg the BIS and the Bank of France).

• A special role for multilateral development banks is warranted, inter alia to support internationally coordinated crisis mitigation public policies, prioritise emergency funding for the poorest countries and evaluate debt sustainability following the crisis.

• Coordination with regulators and the financial sector will also be needed, to study and then develop adequate climate-related prudential regulation as needed.

• Coordination could also extend to standard setters, by considering more “ecological” accounting frameworks, with the possible obligation to disclose additional types of exposure, and new accounting approaches (eg natural capital) to capture interactions between the economy and the natural world. This might necessitate revisiting the many factors that we need to manage to increase the resilience of our global commons.

Should coordination be extended between global agencies that survey macrofinancial stability and agencies that survey other public health vulnerabilities? For climate risks, this would rely on climate scientists and experts in a number of meetings and working groups etc. For pandemics, given their potential real and financial consequences, the issue could be to operationalise an adequate level of cooperation between agencies that assess global macro-financial vulnerabilities and agencies that measure public health vulnerabilities on both the local and the global level (eg more detailed reports on stress tests of health facilities). Should these agencies also have a more systematic relationship with local centres for disease control or CDCs to constantly review their response capacities? Such a closer and systematic relationship would obviously be beneficial if there is appetite to consider building a global safety insurance framework for pandemic risk. Having such resources as a global public good (or at least regional) could perhaps allow a rapid deployment of a massive public health response in the early phases of a disease to mitigate the risk of pandemics. This might also create an incentive for immediate disclosure of any severe epidemic at a local level. Such a framework is obviously not easy to build and it would certainly be costly to keep operational. However, whatever its cost, this would pale into insignificance beside that of the current global sudden stop. The very large economic and human costs already inflicted by the current pandemic are bound to alter our myopic behaviour. Indeed, many countries developed mitigation strategies after SARS but hardly any were implemented. The current crisis may incentivise the building of buffers and the search for insurance.

The huge costs of the current pandemic (see Graph 1) demonstrate the benefits of either some form of ex ante insurance and/or the reinforcement of a medical reserve capacity against potentially devastating future losses. It shows that global negative externalities are not just a hypothetical possibility in the future. Hopefully, this will also undo “the tragedy of the horizon” that leads to procrastination in the fight against climate change. This would serve the purpose of being better prepared, with benefits comparable with those of a Pigovian taxation, as we advocate for greenhouse gas emissions. It could translate into a framework for transfers, taxation and buffers to reduce the risk of such a pandemic. How? By stockpiling the necessary resources and procedures (pandemic health funds, enforceable sanitary regulation, testing processes etc) for prevention. This would be especially critical for low-income countries, but we have seen that it might also apply to some emerging market and advanced economies as well.

4. Does the Covid-19 pandemic look like another Green Swan?

Indeed, the Covid-19 pandemic seems to tick all the boxes defining a Green Swan (see Table 1). It is a global negative externality; it is a global risk with a high or very high probability of occurrence (many scientists have warned us about the possibility of pandemics) and it unleashes multiple non-linear forces that interact with each other, causing severe simultaneous demand and supply shocks. Finally, it puts a significant number of human lives at risk and it requires an unprecedented degree of cooperation to address the problem (no one can hedge such a risk on their own). But beyond that, there climate change and pandemics have connections that can be self-reinforcing (see Box 1). If we recognise such a pandemic as another Green Swan, like climate change, what are the implications?

Green Swans require us to rethink the trade-offs between the efficiency and resilience of our socio-economic systems. In addition to adding global insurance frameworks as described above, one way to address this issue is to think about buffers or some necessary degree of redundancy for absorbing such large shocks. Countries build FX reserves, banks maintain capital buffers as required by regulators, and so on. Perhaps similar “buffers” could be used in other areas of our societies. For example, could it be time to re-assess our production systems, which are meant to be lean and less costly for maximum efficiency?

Yet buffers and redundancies all have a cost. It was decided, for example, post-GFC to build a banking sector with fewer vulnerabilities, more capital and stronger buffers. We already know how to do this for macroeconomic purposes, particularly in terms of fiscal and monetary policy. So could we extend the notion of buffers to climate change and pandemics? The answer to this question will require some thorough assessment. This new approach has already begun to be undertaken by the private sector in re-assessing its own risks and learning lessons from current events, as Covid-19 is affecting global value chains, with a significant local and global impact on services and manufacturing output. Stress tests on their resilience need to be conducted.

Identifying buffers through public expenditure reviews. The urgency of the Covid19 crisis called for a much-needed, timely and aggressive fiscal and para-fiscal response. As a result, Covid-19 has created additional public debt in an unprecedentedly short time span, revisiting Keynes’s question about “how to pay for the war”. After the pandemic peaks, we will have to cope with more debt (see Graph 1) and, at the same time, face greater demand for public goods and, most likely, social demands to even out the distributional effects of Green Swans. Climate-related risks and pandemics have a significant negative redistributive impact. Both risks simultaneously and disproportionately hit the poor in both rich and lower-income countries. Therefore, we need to pay attention to the increase of socio-economic stress in a world that is already fragile and vulnerable. Assessing the sustainability of higher debt levels will be difficult in the absence of a clear picture for future growth. Therefore, if we want to build buffers under severe budget constraints, we will need to conduct more detailed public expenditure reviews to assess our vulnerabilities and the efficiency of public spending, in advanced and emerging market economies alike. Beyond reviewing public expenditure, we may need to confront societal preferences for other means of financing, including taxes, in order to redefine sectoral priorities.

Increasing resilience by revisiting the geography of globalisation. The private sector has made some progress in integrating climate risk into its cost-benefit calculations for locating its facilities and assessing the carbon footprint of its activities. It is likely that it will do the same for pandemics. Progress in logistics and lower transportation costs have made possible just-intime production models with zero stocks. This has greatly increased productivity and allowed production lines to be distributed across the whole planet. But it has also made our economies much less resilient to shocks (no tolerance for disruptions in supply or funding etc). Therefore, many firms will learn from this pandemic in order to become more resilient against future shocks, including climate-related ones. They will start planning alternative locations for their production plants, cut down on business travel, and add more redundancy (in terms of insurance and buffers) that will perhaps increase costs but address these new sources of fragility. Many risks once seen as acceptable will now perhaps be perceived as excessive, based on the impact of Covid-19.

5. Conclusion: “never waste a crisis”

Finally, to conclude, we need to ask how we will extricate ourselves from this crisis without increasing the chances of creating additional climate-related risks. In other words what kind of carbon footprint can we afford to create during the recovery and beyond? Could we engineer a “green” recovery and might we also improve our surveillance of public health conditions globally and locally? As of today, we know that there are several scenarios for the recovery, each with different speeds and patterns. The most likely recovery may include several stop-and-go episodes as emergency measures are relaxed in different countries. But what will its carbon footprint be?

The challenges and complexity of a recovery with a lower carbon footprint are obvious. Understandably, and for good macroeconomic reasons, many countries feel the need to shorten the contraction caused by the lockdown. They are focused on their debt burden, both public and private, which builds up when activity is on hold. Hence the appeal of pushing for the fastest possible recovery while managing the risks that the pandemic will re-emerge.

Moreover, there is tremendous technical uncertainty about the output growth rate during and even after the recovery. Many parameters used to gauge the speed and strength of a standard recovery have most likely changed (owing to factors such as precautionary saving, or peoples’ fear of shopping and participating in production activities), leading to a lack of visibility as to how deep the recession might be and how quickly growth could resume. These uncertainties will also impact inflation, valuation, risk premia and interest rates, among other factors. Perhaps the natural rate of interest (r*) will decline further from its already very low precrisis level. But this is hard to predict. Under these circumstances, adding additional constraints to a recovery plan would not be advisable.

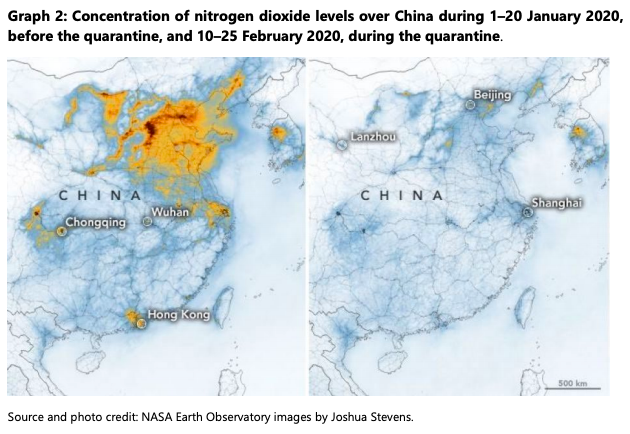

Never waste a crisis. Nevertheless, there has also been an increase in awareness of the immediate reduction in greenhouse gases and other pollutants due to our global sudden stop (see Graph 2). Obviously, no one concerned with social welfare would advocate paying for this reduction by means of a global sudden stop, as a reasonable policy direction for mitigating climate-related risk. However, it is likely that, whatever the shape of the recovery, growth will be subdued for quite a while for the reasons stated above, thereby cutting greenhouse gases emissions and lowering our carbon footprint. In addition, Covid-19 might have presented a vivid image of what the future might look like if nothing is done to reduce greenhouse gases, inflicting similar stoppages worldwide after some tipping-point is reached. It may also have raised awareness of the fragility of some of our systems and therefore of the need for improved efficiency and greater resilience.

Therefore, the Covid-19 crisis might result in a possible shift in the mindset of our societies that could lead to greater acceptance of green policies. This is related to “behavioural contagion theory”. Behaviours may change only if a belief can be backed by a significant amount of evidence. The extreme weather events seen with increasing frequency in the last few years were beginning to persuade people of the dangers posed by climate change. Covid-19 is so overwhelming that it might just have produced this tipping-point where societies begin to fully internalise and understand the danger of complex global risks. If so, it may perhaps bring the political opportunity to further incentivise and then trigger a change in behaviour with a higher probability of success.

It is because of this opportunity that, increasingly, some policymakers are calling for “a green light to lead us on the path of economic recovery”. Indeed, there are some useful policy and institutional lessons to consider if we want to grow again, reduce climate-related risks and improve our resistance to epidemics. If we are not to waste this crisis, reforms will need to result in enduring welfare improvements. In particular, there are calls to take advantage of the existing regional institutional set-ups (eg in Europe) to “share prosperity” during the recovery. In addition to these suggestions, some further elements could help to green the recovery. For example, after the GFC, the bailouts for the automotive industry incentivised it towards producing more electric cars. We have begun to see that teleworking can be effective, so that we can cut out unnecessary trips, thus lowering the carbon footprint of many economic activities. New technologies and changes in the locus of production and work sites could also reduce greenhouse gas emissions. On a broader and more macroeconomic perspective, the recovery may need some heavy lifting to overcome the resistance to change of households and corporates. Massive public investment programmes using, inter alia, MDBs to boost activity could be geared to a global transition to new energies that are less carbon-intensive and to stepping up research in carbon reduction and absorption. Recent studies rank five policies according to both their economic multiplier and their climate impact. It is found that clean physical infrastructure, efficiency retrofits for buildings, investment in education and training, natural capital investment, and clean R&D come top of the list. Last but not least, some major regions could take the lead in promoting both climate-related and public health measures. Regional norms in large markets (such as Europe, China or the Americas) might differ, but if they point in the same direction, they could create market incentives for firms worldwide to enhance or maintain trade relations, and to accelerate the adaptation to a lower carbon economy and improved public health measures at home. Of course these issues are not simple, trade wars could resume, unemployment may increase and other problems may arise. Nevertheless, without at least thinking about these potential new directions, we will miss the opportunity to draw some of the lessons instilled by this very severe crisis.

In order to realise a win-win scenario as a basis for the recovery, we will need to rethink (i) the adequate measurement of global risks; (ii) their proper pricing as negative externalities; and (iii) the resilience of our systems, institutions and modus operandi in avoiding Green Swans. This will require us to look at repricing risk and building buffers as forms of insurance and evaluating the possibility of supplying more global public goods in the area of public health. These measures might appear costly, but the tremendous burden imposed by the current pandemic should be capable of changing our myopic attitudes vis-à-vis Green Swans by incentivising buffers and insurance. We should now have sufficient evidence in front of us to bring home the huge benefits of greater preparedness. Success here will depend on a revival of global multilateral cooperation in managing both climate change and pandemics. It will also entail a redesign of our safety nets and frameworks for aid and global surveillance. For the moment, it seems, one approach to initiating a new way of thinking along these lines would be to build on or expand an existing “coalition of the willing” of both public and private actors (including large corporations that are sensitive to these risks). And we should start this work immediately, since as the great poet Antonio Machado said: “Caminante no hay camino, se hace camino al andar” or “Walker, there is no road. The road is made as you walk.”

These remarks result from work with my Green Swan co-authors, Patrick Bolton, Morgan Després, Frédéric Samama and Romain Svartzman, respectively from Columbia University, Bank of France, Amundi and Bank of France. We would like to thank without implicating Laurence Boone, Benoît Cœuré, Torsten Ehlers, Jean-Pierre Landau, Benoît Mojon and Előd Takáts and participants at the OECD and BIS Webinars for useful comments. Thanks also to Teuta Turani for excellent research assistance. The views expressed here are our own and do not necessarily represent those of our institutions.

Luiz Awazu Pereira da Silva, Deputy General Manager of the Bank for International Settlements (BIS).

__________________________________________________

Source: https://www.bis.org/speeches/sp200514.htm

P Bolton, M Després, L Pereira da Silva, F Samama and R Svartzman, The green swan – Central banking and financial stability in the age of climate change, Bank for International Settlements and Bank of France, 2020.

Président de l'association

Président de l'association